As economic uncertainty rises and recession forecasts become more prominent, many are questioning how this might ripple through the housing market. While recessions typically bring financial turbulence, they can also shift market dynamics in ways that offer both risks and opportunities—particularly for homebuyers, sellers, and investors.

Why It Matters

The housing market is a key pillar of the U.S. economy, and its performance affects millions of Americans—whether they own a home, are looking to buy, or rent. A slowdown or price correction can influence everything from family finances to national economic growth. Understanding how a recession might impact real estate helps consumers make better decisions, avoid panic, and take advantage of strategic opportunities.

Additionally, real estate trends often reflect broader shifts in consumer confidence, employment, and lending conditions. For that reason, the housing market is frequently viewed as a barometer for the overall health of the economy.

Mortgage Rates Could Trend Downward

Historically, mortgage rates tend to fall during recessions. This is largely because investors move money into safer assets like U.S. Treasury bonds, which lowers yields and, in turn, brings mortgage rates down. In early April 2024, the 30-year fixed-rate mortgage dipped to 6.64%, the lowest level in six months. Should recessionary pressures intensify, rates may drop even further, enhancing affordability for qualified buyers.

Softening Buyer Demand May Ease Home Prices

A recession typically reduces household confidence and purchasing power, causing many potential buyers to delay major financial decisions. This decline in demand often leads sellers to lower asking prices to attract a limited pool of buyers. However, experts suggest any drop in home prices is likely to be modest due to the persistent housing shortage across the U.S. and historically low mortgage delinquency rates.

Construction Activity May Slow

Recessions usually discourage new construction. Builders, facing higher material costs and waning demand, often scale back housing starts. While this helps balance short-term supply with demand, it could exacerbate long-term inventory shortages. That means even if prices soften temporarily, a lack of new homes could push them back up once the economy rebounds.

Access to Credit Could Tighten

One side effect of recessions is that lenders often become more conservative. Even with lower mortgage rates, qualifying for a home loan may become more difficult as banks impose stricter lending criteria. Higher unemployment and economic volatility further complicate the mortgage approval process, sidelining many would-be buyers.

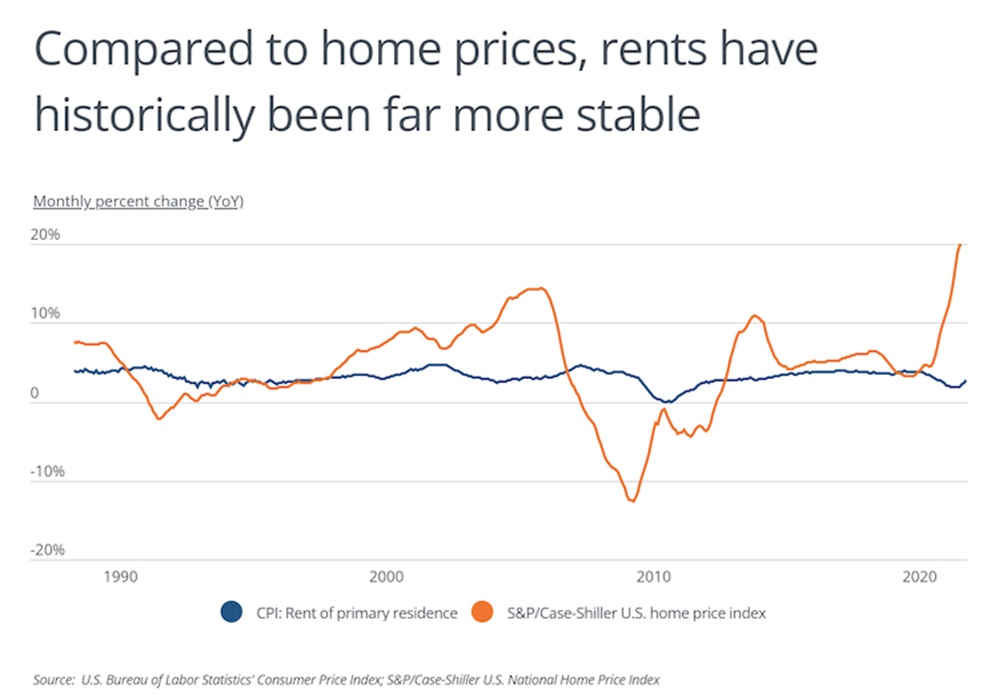

Rental Market Stability May Rise

In times of economic downturn, renters are more likely to stay put rather than pursue homeownership. This trend could stabilize the rental market, keeping occupancy rates high while reducing tenant turnover. For landlords and property investors, this might translate to consistent rental income even amid a slowdown in property sales.

What Buyers and Sellers Should Keep in Mind

For buyers, a recession can present a window of opportunity—particularly if mortgage rates drop and sellers become more flexible. However, financial stability is critical. Lenders may favor borrowers with strong credit and steady employment, so preparing financially is essential.

Sellers, on the other hand, should be ready for a slower market. Pricing homes competitively and being open to negotiation will be key to attracting serious buyers. Patience and market awareness can make the difference between a successful sale and an extended listing.

Investors may also find opportunities, especially in rental properties or undervalued markets, but must factor in potential shifts in tenant behavior, construction delays, or tighter credit conditions.

A Balanced Yet Cautious Market

While a potential recession could cool parts of the housing market, particularly through decreased buyer activity and restrained homebuilding, the overall outlook is more balanced than bleak. Real estate continues to offer stability for many investors, and some experts believe housing may even outperform other sectors during a downturn. Goldman Sachs, for instance, recently raised the probability of a U.S. recession to 45%, while J.P. Morgan set it even higher at 60%.

Ultimately, those who stay informed and agile will be best positioned to navigate the shifts ahead.